From 1 July 2026, the way employers pay Superannuation Guarantee (SG) is set to change significantly. If you run a small business, this will impact your payroll processes and cash flow management.

Here’s what you need to know and how to prepare.

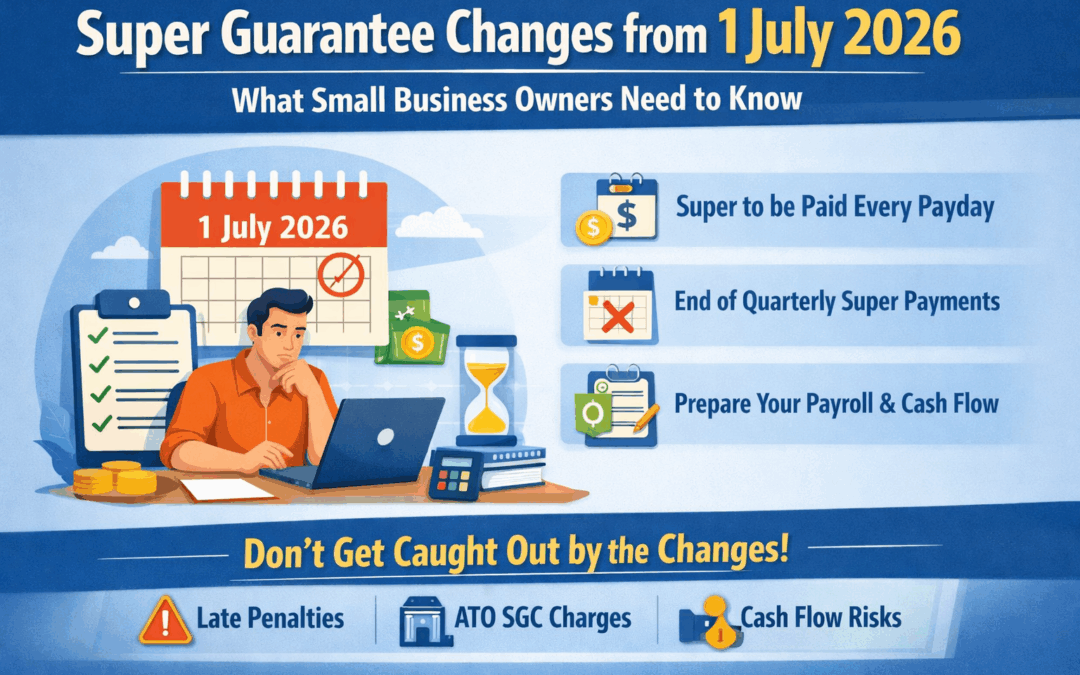

What’s Changing?

Currently, employers are required to pay superannuation contributions at least quarterly.

From 1 July 2026, employers will be required to pay Super Guarantee at the same time as wages, effectively moving to a “payday super” system.

This means:

- Super will need to be paid each pay cycle (weekly, fortnightly or monthly)

- Quarterly super payments will no longer be compliant

- Payroll systems will need to process super automatically with wages

Why Is This Happening?

The government’s objective is to:

- Ensure employees receive their super sooner

- Reduce unpaid super liabilities

- Improve transparency and compliance

While this is positive for employees, it will require businesses to tighten their payroll systems and cash flow management.

How This Will Impact Small Business

For many small businesses, super is currently managed quarterly, which allows some flexibility in cash flow.

Under the new rules:

- You won’t be able to “hold” super until the quarterly due date

- Super becomes an immediate payroll cost

- Cash flow pressure may increase, particularly for labour-intensive businesses

If your business operates on tight margins or irregular cash flow, this change needs planning now, not in June 2026.

What You Should Do Now

Although the change doesn’t start until July 2026, preparation should begin well before then.

1. Review Your Payroll Software

Ensure your payroll system (e.g. Xero, MYOB, etc.) is set up to process super each pay cycle.

2. Adjust Cash Flow Forecasting

Update your forecasts to reflect super being paid with wages rather than quarterly.

3. Tighten Internal Processes

Make sure wage payments, STP reporting, and super processing are aligned and automated.

4. Address Any Existing Super Issues

If you currently have unpaid super or an ATO SGC debt, this change makes compliance even more critical.

What Happens If You Don’t Comply?

Late or unpaid super can result in:

- Super Guarantee Charge (SGC)

- Interest and penalties

- Loss of tax deductibility of super payments

- Director penalty notices in certain circumstances

The ATO is increasing its data-matching capabilities, and payroll reporting is already real-time through Single Touch Payroll.

In short, this is not an area to fall behind on.

Final Thoughts

The move to payday super is one of the biggest payroll compliance changes in recent years.

While July 2026 may seem some time away, small business owners who prepare early will avoid unnecessary stress, cash flow shocks, and potential penalties.

If you would like assistance reviewing your payroll setup or cash flow planning in light of these changes, please feel free to contact our office.